Portfolio Power Tools: Diversification, Asset Allocation, and Rebalancing

Y'all know about power tools. Those are the tools that magnify what you might do manually. Often, they allow you to do things that couldn't be done any other way. Here are three portfolio power tools that are safe, efficient, effective, inexpensive, and easy to use.

Diversification

Asset Allocation

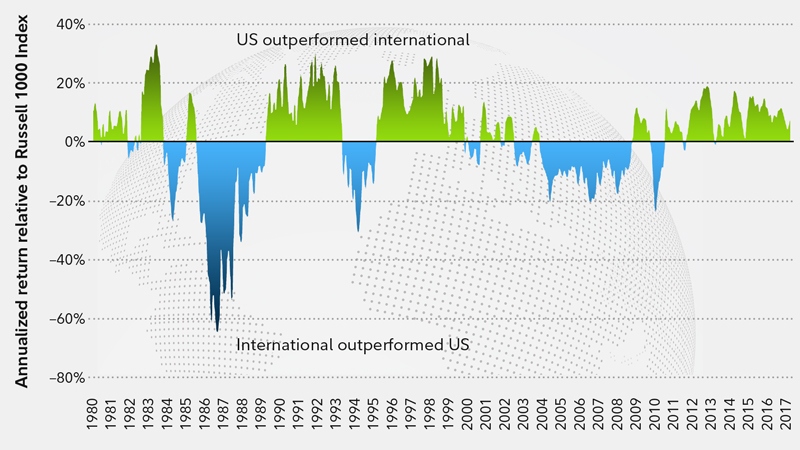

Diversification means that different kinds of investments are held in many countries, roughly in proportion to the size of the markets they represent.

For

example, the US has the largest single-country representation of stocks with

about 55% of global assets. The other 45% is spread across all the other

countries with Japan, China, Hong Kong, the UK and Europe comprising

the largest segments.

Diversification

also means holding investments in smaller companies as well as the

behemoths, and across all major industries. While the behemoths represent about 70% of global markets, diversification benefits can be realized by holding mid and small-sized companies. Hence, a total stock market fund would be a more diverse holding than an S&P500 fund.

Holding three major bank funds or ETFs is not diversification. Neither is hanging on to your company's stock because you're so loyal.

In the bond market, diversification means holding a spectrum of maturities from short to long, and a spectrum of quality from AAA to junk.

Holding three major bank funds or ETFs is not diversification. Neither is hanging on to your company's stock because you're so loyal.

In the bond market, diversification means holding a spectrum of maturities from short to long, and a spectrum of quality from AAA to junk.

Diversification

reduces portfolio volatility. The major advantage of this is that it

makes it easier to stick with a portfolio in high-stress markets.

Diversification helps manage non-systemic and systemic risk. That's geeky jargon for risks that can be minimized and risks that are simply unavoidable.

Non-systemic

risk is company-specific risk. It's the risk that batteries catch fire,

food is tainted, proprietary computer systems are hacked. This risk is

avoidable. Just own a lot of different companies. While a few may be spectacular failures and others equally spectacular successes, the

entire package remains viable.

Systemic risk

is market-specific risk. It's the risk that remains after non-systemic

risk is diversified away. Think of it as "market risk"-- the risk of

overall market chaos and dysfunction. It's the risk that appeared in 2008. This risk

cannot be diversified away; it is a market feature. The only way to

avoid it is not to invest there.

Reference:

How does diversification actually work? Bob French, CFA

There are only two major asset classes that comprise most security-based* investment portfolios: equities (stocks) and fixed income (bonds). Everything else is a sub-class of those two things. "Cash" itself is a high quality, short-duration class of fixed income.

Asset allocation is the result of deciding how much of the portfolio to put in each asset class. This is not hard to do. Effective global asset allocation can actually be accomplished with one fund.

Factors that come into play when deciding on allocating assets are:

Asset allocation is the result of deciding how much of the portfolio to put in each asset class. This is not hard to do. Effective global asset allocation can actually be accomplished with one fund.

Factors that come into play when deciding on allocating assets are:

- Desired returns. Higher returns require a greater allocation to stocks; more modest returns, more bonds.

- Willingness to endure price volatility. More willingness allows for more equities; less willingness, more fixed income.

- How long it will be until the money is used. Sometimes this is called timeframe. Our Five-Year Rule says that any money earmarked for use within five-years must be invested in a bond asset class. Conversely, 100% of any money earmarked for use beyond five-years can be invested in stocks.

Rebalancing

Rebalancing is when adjustments are made to a portfolio in order to hew it closely (within 5%-10%) to its intended asset allocation. Three things might lead to a rebalancing action:

1. Large portfolio withdrawals.

2. Large portfolio additions.

3. Significant outperformance or underperformance occurred in one or more asset classes.

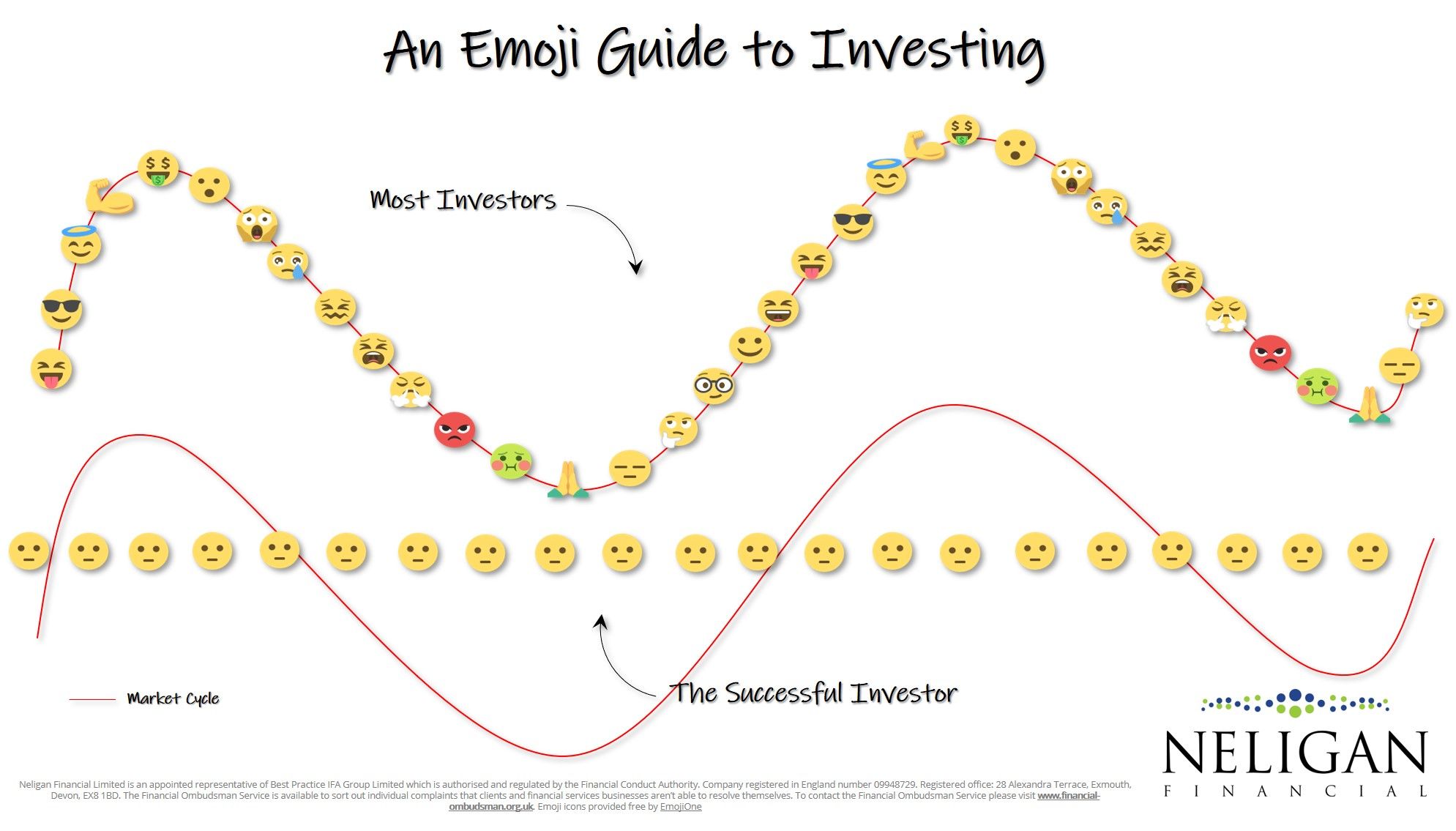

A Vanguard paper concluded that more frequent rebalancing is not especially productive, and that even a policy of not rebalancing is a viable strategy. There's even a thing called "rebalance timing luck." The robo-adviser industry hype of frequent rebalancing is fluff; it's main purpose is to impress you that they're doing something to your great advantage.

There's no point in making this more complicated than necessary. Like most things, simple beats complex; less tinkering leads to better results. Don't just do something; sit there.

A 2017 paper titled Vanguard's Framework for Constructing Globally Diversified Portfolios provides a more detailed treatment of these power tools.

Rebalancing is when adjustments are made to a portfolio in order to hew it closely (within 5%-10%) to its intended asset allocation. Three things might lead to a rebalancing action:

1. Large portfolio withdrawals.

2. Large portfolio additions.

3. Significant outperformance or underperformance occurred in one or more asset classes.

A Vanguard paper concluded that more frequent rebalancing is not especially productive, and that even a policy of not rebalancing is a viable strategy. There's even a thing called "rebalance timing luck." The robo-adviser industry hype of frequent rebalancing is fluff; it's main purpose is to impress you that they're doing something to your great advantage.

There's no point in making this more complicated than necessary. Like most things, simple beats complex; less tinkering leads to better results. Don't just do something; sit there.

A 2017 paper titled Vanguard's Framework for Constructing Globally Diversified Portfolios provides a more detailed treatment of these power tools.